Recap from Part II – Money and Money Things

In the previous part, Money and Money Things, we have gone through the following topics:

- The origin and evolution of money according to the traditional and the modern money view.

- What is money and why is accepted.

- Difference between Money and Money Things.

- Different currency regimes.

Highlights of Part III – Sovereign Government and Fiscal Policy:

After having defined what a (full) sovereign country is, we delve into the operations of spending, taxation and deficit in modern money environment.

Fiscal policy for a sovereign country (spending and taxation)

Sovereignty and Money

Before going through the details of the fiscal policy conducted by the central governments, we need to define a sovereignty scale. As mentioned in the previous part, Money and Money Things, the monetary regime plays a paramount role in determining the policy space and the fiscal policy of a State.

Based on the monetary regime I have defined 3 sovereignty degrees:

- Full Sovereign country:

- A country whose central government issues its own unpegged and non-convertible currency which is used as domestic unit of account.

- Sovereign Country:

- A country whose central government issues its own currency which is used as domestic unit of account.

- Non-Sovereign Country:

- A country whose central government uses as domestic unit of account a currency issued by a foreign entity.

The difference between Full Sovereign country and Sovereign country (non Full) is the existence of a peg on the national currency, while the former issues a floating non-convertible currency (fiat money) the latter issues a pegged currency.

Countries that adopt a fixed exchange rate cannot be considered fully sovereign due to the fact that the peg introduces restrictions on their policy space (spending constraints and default risk).

Non-Sovereign countries lies on the lower level of the sovereignty scale since they do not issue their domestic currency, but use the money issued by a foreign country. They adopt the hardest form of peg.

Their policy space is even more restricted than the non-full Sovereign Countries and are subject to budget constraints like any other private sector actor.

Sweden and USA for instance are Full Sovereign while all the Euro-countries are Non-Sovereign.

NB

From this point onward everything I say regarding fiscal and monetary policy is referred to Full Sovereign countries unless otherwise specified.

You can notice the emphasis that I put on the words “issue” and “use”. There is often some confusion, especially regarding domestic fiscal policies, between the issuer and user of money.

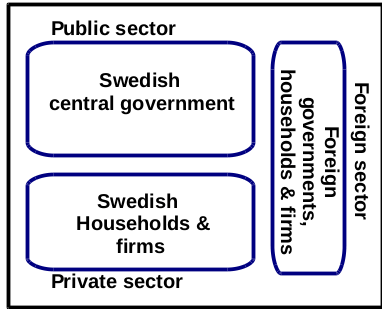

In the sectoral balances approach introduced in Part I we have identified 3 sectors forming the whole macroeconomic world: domestic public, domestic private and foreign sector. Based on a domestic policy perspective, which one is the issuer and which the user?

Let’s say that we are discussing economic policy in Sweden, so the domestic public sector is the Swedish central government, the domestic private is composed by Swedish households and firms (profit and no-profit) and the foreign includes everything outside the Swedish jurisdiction.

Central government is the sole issuer of the money: the government creates money from nothing, it spends money into existence.

The domestic private sector is a mere user: it can only use the money that has been already issued, spent, by the central government.

Though it is true that bank can create money, remember that banks create money things not money, see Part II.

The foreign sector is a user like the domestic private sector: the rest of the world cannot issue the Swedish national currency, it can only use it.

These conclusions apply for Sweden since its national currency is unpegged and non-convertible (fiat).

Would these apply for Italy or Spain?

Unfortunately not, Italy and Spain are jailed in the Euro zone and they cannot issue Euro. The money they need for economic policies must be borrowed from a supranational entity, the European Central Bank.

The ECB is the issuer of the Euro which is the only social unit of account used in all the Euro countries, thus domestic central governments are on the same level of households and families, they are users.

Now we are ready to enter the realm of fiscal policies and analyse what the wrong and correct approaches are when running the fiscal policy for a full sovereign country.

Wrong approach to fiscal policy

- Spending

- Government has budget constraints, like households and firms

- Government spending must be funded through taxation or borrowing (bond sales)

- Spending comes after taxation

- Taxation

- Taxes finance government spending

- Taxation has to come before spending

- Deficit

- Government deficit is the private sector burden

- Deficit drives interest rates up, takes away private saving and generates inflation

- Today’s deficit is the future generations’ burden

Correct approach to fiscal policy

- Spending

- The government can always afford to buy what is on sale in its own unit of account

- As the sole manufacturer of the currency the government can never become insolvent

- Spending comes before taxation

- Taxation

- Taxes cannot finance government spending

- Taxation occurs after spending

- Taxes exist for a monetary purpose not for financing (same applies for bond sales)

- Deficit

- Government deficit is the private sector net wealth

- Today’s deficit are the future generations’ savings

Let’s analyse each element (spending, taxation and deficit) and explain why the first approach is wrong while the second is correct.

At this point is important to have clear in mind the functioning of a modern monetary system, in particular how money is created and the role of taxation in its acceptance, these topics have been covered in Part II.

Spending and Taxation

Government spending creates money.

Spending is the process through which the central government introduces liquidity, money, in the system.

It spends money into existence by crediting bank reserves, in earlier time this was achieved by printing money while today is mainly a keystroke.

The money comes from nothing, it doesn’t come from taxation or other financing vectors (like treasury bonds sales), the government simply creates it.

Ben Bernanke interviewed by Scott Pelley: Bernanke explains where the money came from for the 2009 banks bailout. It’s not taxpayer’s money, they just printed it.

https://www.youtube.com/watch?v=U_bjDAZazWU.

As the sole manufacturer of money, the sovereign government can never run out of money and never become insolvent on liabilities denominated in its money of account (national currency).

It follows that the default probability of the government on an exposure denominated in domestic currency is zero.

Let’s go back to Sweden; what is the probability that the Swedish government will become insolvent on its obligations? It depends.

- If the exposure is denominated in US Dollar or British Pound than the probability of default is very low (Sweden is AAA rated by the way) yet not 0.

- If the exposure is denominated in Swedish Crown than the probability of default is 0.

Where is the difference?

In the first case the government has a debt in a currency that it cannot issue but only use; Sweden cannot emit Dollar or Pound hence there is a probability, even though is very low, that the government won’t be able to obtain the foreign currency (Dollar or Pound) needed to repay the debt.

In the second case, the government has an exposure denominated in the domestic unit of account (Swedish Crown); in this case, Sweden is the issuer of the currency and it can never be forced into default since it can keystroke as many Swedish Crown with virtually no limitations. The probability of default is 0.

Alan Greenspan vs Paul Ryan on USA solvency:

https://www.youtube.com/watch?v=DNCZHAQnfGU

From the St. Louis Fed:

“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Taxation cannot precede spending.

Remember from the history of the evolution of modern money, the centre had to give the tokens (spend) to the people before it could collect them (tax).

The same logic applies in today’s society, money is made available to the private sector by the government spending. The government introduces money in the private sector (spending) and only successively it may, eventually, drain some of this money (taxation).

The private sector cannot pay any taxes if it haven’t received any money yet!

Implying that the government needs tax money to finance its spending is absurd, since:

- It is the sole manufacturer of money: the private sector, the tax payer, cannot issue money hence the only way it can pay any taxes it to use the money previously spent by the government.

- It cannot borrow its own IOUs: the government cannot borrow from itself.

- Spending must precede taxation.

The role of taxation

We have seen that taxes do not finance government spending and the spending precedes taxation.

So why do we have to pay taxes? Can we remove taxes completely?

Taxation is primarily a monetary operation and not a financing source, for a sovereign government.

Real purposes of taxation:

- Taxes drive money: taxation ensures a demand for the national currency

- Control of inflation

- Reallocation of national wealth

- Constrain over-accumulation of wealth

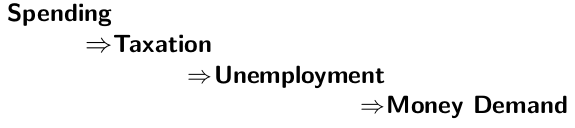

Taxes drive money

Remember from the history of money presented in Part I, when the centre issued the tokens it also imposed a tax, to be paid only with the tokens, in order to ensure the people will accept them.

The imposition, by the government, of a tax liability to be paid in the national currency ensures a demand for this currency.

The fundamental link between Taxation and Money Demand is Unemployment.

Interactive example.

I am now going to explain you how taxation and money demand are linked through unemployment. I do it by an interactive example (thank you Warren Mosler).

Imagine the situation. You go the cinema, buy your popcorn, enter the hall and take your sit. The hall is full, 100 people.

Lights off.

Everyone expects the movie to begin but it doesn’t, instead the lights are turned on again and I appear, standing on the scene, right in front of the first row.

Bewildered people started to murmur until I start talking.

“OK, ladies and gentlemen, listen up. My name is Fausto and from this moment I am your king. This movie hall from now doesn’t belong to Sweden any more, it is an independent nation.”

The murmurs turn to laughter but I carry on.

“I want anyone who is unemployed to raise the right hand.”

No hands are risen, so everyone is employed, good.

“Pay attention now. Since this is my nation I dictate the rules. There is lots of work to do in this hall and I need workers. Workers are required for replacing all the light bulbs, repairing the ceiling, cleaning the floor and repainting the walls.

As compensation for you work I will pay you the sum of three Gils”

Someone from the hall ask me what a Gil is.

“A Gil is the currency of this nation, it is basically only a piece of paper with my signature on it, nonetheless it is the only legal money accepted here.”

“So, how many of you want to work for me?”

As expected, no one raises the hand. They are not going to work for me since they all already have a job and more important they are not interested in getting paid in a currency without value for them (the Gil).

“Well, I expected that, no one wants to work for me. But I forgot to tell you something; you see, this hall is sealed from the inside and there is only one way out off here which is the door on my left. Unless you can walk through walls that door is your only way out.”

I point at the door and a man with a shotgun appears right in front of it.

“Let me introduce Barret, he is a soldier and works for me. Here is the situation, if you try to exit the hall through the door, Barret will ask you 1 Gil, if you don’t give him you will be shouted on the spot. A the end of the day Barret will come to each of you and collect 1 Gil, if you don’t give him your are dead.

And just to make things clear, Barret accepts only Gils, no Swedish crown, no dollars, nothing but Gils”

“Let me ask you one more time. Does anyone want to work for me and get paid 3 Gil?”

Guess what, everyone raises his hand now.

What did just happen?

The people in the room were not unemployed because the had a salary in Swedish crown and they paid taxes in the same currency.

Things changed when, I, the king, imposed a tax (1 Gil).

From the moment I imposed a new tax in another currency they didn’t hold the situation changed radically. Everyone became unemployed and in desperate need to get the Gils needed to pay my tax.

Now everyone wants Gils because they need them to pay taxes.

So, the tax imposition generated unemployment which created a demand for the money.

Control of Inflation

Taxation sets an implicit floor to the value of domestic currency, a minimum level of demand that keeps the price above 0.

Should the inflation reach extremely high levels (hyperinflation), money’s value will fall very quick and the population could refrain from holding the domestic currency as unit of account.

Taxation and inflation:

- Higher taxes → lower inflation

- the government drains more money from the private sector

- the private sector has less money in circulation prices tend to decrease

- Lower taxes → higher inflation

- the government spends more in the private sector

- money circulation in the private sector increases

- prices tend to increase.

Fiscal policy is much more effective for controlling the inflation than the monetary policy.

Government Borrowing.

Link between the Central Bank interest rate target and the government spending:

- Government spending adds extra reserves to banking system

- Interest rate declines (under the CB target) as the quantity of reserves increases

- Government drains excess reserves by selling securities → Borrowing

- Interest rate re-aligns with the Central Bank target

Why would banks buy the securities the government is selling?

It is an opportunity cost:

- Excess reserves pays 0% interest rate (normally)

- Government bonds have a positive interest rate.

Government borrowing is a monetary operation (support interest rate) and not a financing fiscal operation.

Government deficit policies

The Government budget policy:

- Government Deficit → private sector net wealth is positive → the private sector is saving

- Government Balanced → private sector net wealth is zero → the private sector gets nothing

- Government Surplus → private sector net wealth is negative → the private sector goes into deficit.

In order to explain the three budget policies I make the assumption the foreign sector (or current account) is in balance, import equals export. We will then focus on the interaction between the domestic public and private sector.

In the next paragraph I will reintroduce the foreign sector and demonstrate its incidence on the two domestic balances.

Sectoral balances with foreign sector in balance

Government Net Lending = Private Sector Net Financial Wealth

OR

Public Deficit = Private Surplus

Government Deficit – Optimal

Stage 1:

- government spends money into the system

the government goes into deficit

the government goes into deficit- the private sector gets the money and goes in surplus.

Stage 2 – optimal:

- government claims only part of the money it had spent

- the government remains into deficit

- the private sector stays in surplus

- the private sector accumulates net wealth (net saving)

Government Deficit – Bad

Stage 1:

- government spends money into the system

- the government goes into deficit

- the private sector gets the money and goes in surplus.

Stage 2 – bad:

- government claims all the money it had spent

- the government balances its budget

- the private sector gets nothing

Government Deficit – Worst

Stage 1:

- government spends money into the system

- the government goes into deficit

- the private sector gets the money and goes in surplus.

Stage 2 – worst:

- government claims more money than it had spent

- the government goes into surplus

- the private sector needs to either borrow or dissave in order to pay taxes

- the private sector goes into deficit

- the private sector accumulates debt (wealth destruction)

Budget Deficits and Interest Rates

We have seen how the deficit of the government affects the private sector net wealth. But what happens to the financial market? Does an increase of the government deficit automatically leads to an interest rate raise?

As usual, when dealing with monetary policy, it depends on the monetary sovereignty of the state (don’t forget the sovereignty scale we defined above).

For non-sovereign countries it usually does since an increase in deficit can lead to solvency problems, hence the interest rate can increase because of the higher default risk.

For sovereign countries (non full), the higher deficit can push the interest rate up if there is a risk that the government will not be able to maintain the peg.

For full-sovereign countries higher deficit does not normally generate an increase of the interest rate, as long as the central government and the central bank coordinate properly.

This is how central bank and government coordinate.

- Deficit spending generates excess reserves in the private banking sector

- Private banks seek to lend the excess reserves in the overnight interbank lending market

- Extra supply of reserves pushes the overnight interbank lending rate below its target

- Excess reserves must be drained in order to keep the interest rate in line with the target, this generates 2 scenarios :

- One:

- Central Bank intervenes to remove excess reserves

- Private banks seek a more profitable alternative to reserves.

- Two:

- Central Bank sells treasury bonds from its stock to private banks (Open Market Sale)

- The treasury sells bonds directly through the bond market

- One:

- The Interest Rate re-aligns to its target

Government Deficit policies and the Foreign Sector

Sectoral balances with foreign sector positive/negative

Government Net Lending = Private Sector Net Financial Wealth ± Foreign Net position

OR

Public Deficit = Private Surplus ± Current account

The Foreign Sector (Current Account) role:

To support the private sector when the government runs a budget surplus (or balanced).

Export is a survival element for countries whose government runs tight fiscal policy (look at the Euro zone).

We have seen that when the government balances (or goes plus) its budget the private sector gets nothing (or minus). The money inflow coming from the export supplies the private sector with extra financial wealth.

The export works as a support to the private sector balance, it is what prevents households and companies to be in financial stress.

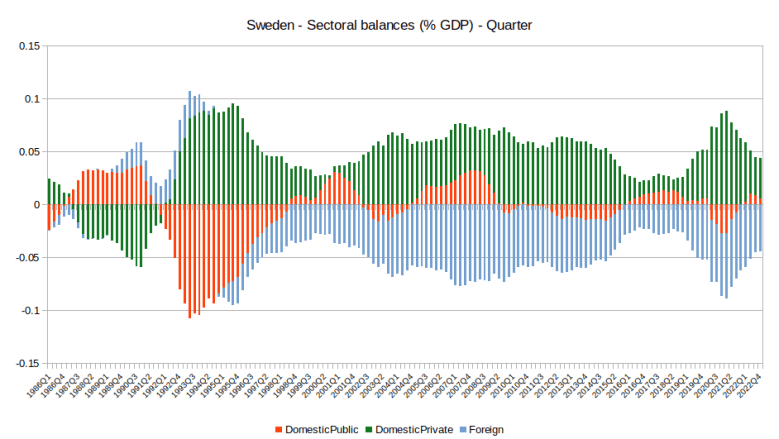

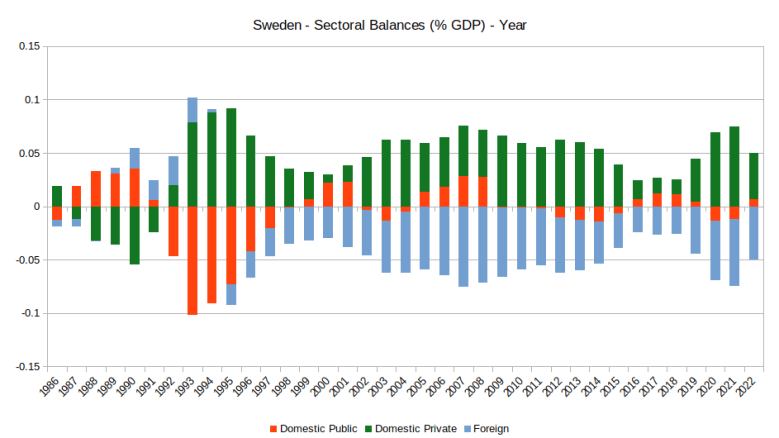

Sweden is a sad example of this, the tight fiscal of the last years has drained a lot of wealth from the private sector. Without the inflows coming from the export the private sector would have collapsed (look at the graph below – Sweden sectoral balances).

This is not an optimal condition, a country dependent on export is implicitly constraining the domestic economy to the fiscal policy of a foreign country.

To increase budget deficit when the private sector is in surplus.

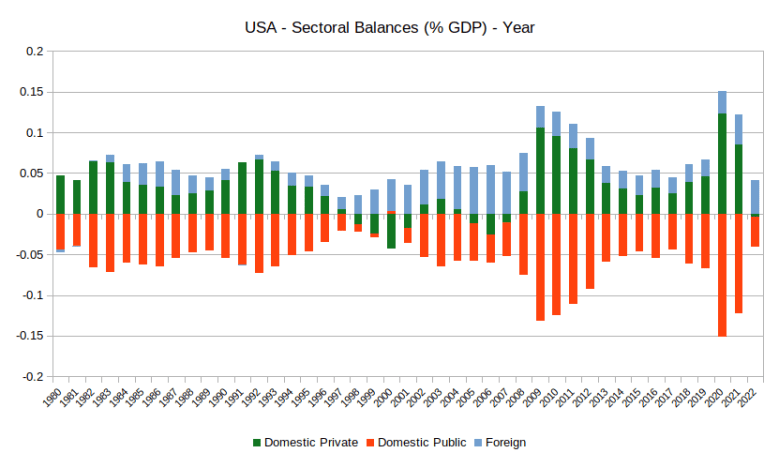

Here we have the opposite situation, when the government deficit is positive and the private sector is better off, import generates an outflow of money that will increase the government spending. This is the case of the USA, look at the graph below – USA Sectoral Balances.

Government spending increases either directly or indirectly.

If the government starts to import more than it exports the deficit will directly increase.

If the import impulse comes from the private sector then the deficit spending will indirectly increase since the government has to increase its deficit in order to keep the private balance positive.

Analysing the most important graph

The graphs reported down have been introduced in Part I – Macro Fundamentals as the “most important graphs”, here we look closely and them and draw some conclusions upon.

Each plot depicts the 3 balances, in % GDP, on early basis.

The feature that should come to your eyes first is the shape of the graphs, a mirror, with symmetry axes on the 0 line.

Why a mirror?

It is because the sum of the 3 balances is always zero, we have gone through this in the previous parts and here you have a real proof.

Look the USA example.

The red bars represent the Government Balance, if they are below 0 it means the government is running a deficit, surplus if they are above 0.

The green bars represent the private sector balance, below 0 is deficit and above is surplus.

The blue bars are the foreign balance, it they are above the 0 the rest of the world is running a surplus, hence USA is importing more than it is exporting; vice versa if they are below 0, exports greater than imports.

As we can see USA has been a net importer for the last 20 years (blue bars above 0).

It is the private balance that is more interesting, it has been positive until 1997 before going in deep deficit. The balance became negative due to a tightening of the government fiscal policy (Clinton’s plan to balance the federal budget). The government went plus and determined a deterioration of private net wealth that didn’t fully recovered until 2010.

Government Deficit – USA Sectoral Balances

I produced the same graphs for Sweden (they are the same, one is with bars and one with line), all data is available from the Swedish central statistics bureau (Statistics Sweden).

In Sweden the private sector economy has been regularly attacked over the last decade. You can clearly see that every time the government deficit decreases the private sector loses wealth (1998, 2006, 2016).

What is preventing the Swedish economy to collapse? The foreign sector (remember when I said that export can support the private balance when the government is tightening?).

The Swedish foreign sector is constantly in deficit hence export exceeds import (check the blue bars).

Without the wealth inflow coming from the rest of the world Swedish households and firms would be in serious economic distress.

The graph proves another important as well as worrisome evidence, until 2019 the Swedish government was maintaining a tight fiscal policy while the export sector was shrinking (you can see the blue bars/line trend going slowly toward 0).

This was basically a nice way to destroy a country, tighten the fiscal policy and leave the private sector net wealth in the hand of the rest of the world fiscal policy.

What was the result of this suicidal policies? Persistent low inflation and increasing indebtedness among Swedish households and firms.

Government Deficit – Sweden Sectoral Balances

References for part III:

Bell, S.A. (2000) Do Taxes and Bonds Finance Government Spending? Journal of Economic Issues, 34 (3): 603-620

Bougrine, H. and Seccareccia, M. (2002) Money, Taxes, Public Spending, and the State within a Circuitist Perspective, International Journal of Political Economy 32 (3): 58-79.

Fiebiger, B. (2012a) Modern Money Theory and the Real-World Accounting of 1-1¡0: The U.S. Treasury Does Not Spend as per a Bank. Political Economy Research Institute Working Paper No. 279. Amherst: University of Massachusets Amherst

Kelton S. (2020), The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy, Public Affairs

Keynes, J.M. (1964). The General Theory, New York: Harcourt-Brace-Jovanovich.

Mosler, W., 1995. Soft Currency Economics, 3rd edition. West Palm Beach, FL (self-published). Http: http://www.warrenmosler.com.

Mosler, W. 2010. The Seven Deadly Innocent Frauds of Economic Policy, Valence Co., Inc.

Tymoigne, E. (2013) Modern Money Theory, and Interrelations between Treasury and the Central Bank: The Case of the United States, mimeograph.

Tymoigne, E. and Wray, L.R. (2013) The Rise and Fall of Money Manager Capitalism. London: Routledge.

Wray, L.R. (2012) Modern Money Theory: A Primer on Macroeconomics for Sovereign Monetary Systems. New York: Palgrave.