Recap from Part I – Macroeconomics Fundamentals

In the previous part, Macroeconomics Fundamentals, we have gone through the following topics:

- The key differences between Orthodox and Heterodox macroeconomics.

- The 3 sectors forming the macroeconomic environment: domestic public, domestic private and foreign.

- The sectoral balances and the stock-flow consistency: one sector’s deficit corresponds to the surplus of the other.

Highlights of Part II – Money and Money Things

In this second part, Money and Money Things, we start with the evolution of Money from primitive society to contemporary era (traditional and modern money view), followed by the different views on money by Orthodox and Heterodox macroeconomics.

The last section focuses on the difference between Money and Money Things along side the different currency regimes.

Origin and evolution of Money

The origin of money according to the traditional view.

Money as a medium of exchange

The barter.

It all starts in a primitive society, essentially a subsistence society where individuals exchange goods needed mainly for sustenance. In this society the only type of exchange is the barter since there is neither money nor unit of accounts.

With the advancement of the society the barter becomes increasingly inefficient.

One reason is the mismatching preferences of the individuals, if one wants to exchange two sheeps for a cow one needs to find, at the same time, someone who owns a cow and is willing to have sheeps.

Another reason is the difficulty to operate barter between groups, mainly because the goods object of the exchange can be difficult to divide.

It becomes evident that the society ought to find an alternative, more efficient, way to run the raising market economy.

Gold and Goldsmiths.

The society increasingly find metals to be particularly suitable for its trading activities, especially one metal, gold.

Gold becomes the preferred metal used as a medium of exchange: it was attractive, very valuable even in very small quantity and easily divisible.

People begin to make small pieces out of gold, the coins, and when the coinage activities grow in relevance the government steps in and starts producing the coins in a more convenient and efficient way.

Gold has nonetheless a major problem related to its intrinsic value, it needs to be protected.

This protection task is taken over by the goldsmiths that step in as safe-keepers of the gold.

Banks and Government.

An individual possessing a given amount of gold and wanting to keep it safe can go to a goldsmith and make a deposit. The goldsmith issues a receipt as proof of the gold deposit.

Goldsmiths soon realise that the probability that all the depositors turn to them and retire all their gold deposits on the same day is very low. They then start to issue more receipts than held gold deposits and these receipts become a new medium of exchange.

Goldsmiths develops into financial actors, banks are born.

The primary function of the newly born banks is in fact the multiplication of the amount of medium of exchanges (money).

The government comes in, again with a support role, as a lender of last resort to stabilise the system.

The origin of money according to the Modern Money view

Money as a social unit of account

The groups.

It starts in a primitive society with no unit of accounts and no money and the barter is the only type of exchange.

With the advancement of the society people started to organise and live in groups. The survival of a group depends primarily on people contributions. Each member of the group must fulfill certain duties, like food production (harvesting), defence (military service) or building/maintenance activities.

These contributions are made in kind since there is no unit of account hence no liquidity. The tasks are usually assigned at fixed time; for example, the group leader decides that each January, every man is required to help reinforcing the village outer fence.

There are however situation when the duties can be required before the scheduled time. If, for instance, the nearby village starts to get too aggressive then the group leader would require the construction of a new fence in September instead of January.

When contributions are made ahead of time the leader of the group gives out a “token”. People who fulfills a duty on centre’s demand receive a token. This token can later be given back to the centre and it will grant an exemption from that duty.

Alternatively, the token can be passed through other members of the group in exchange of goods.

The tokens issued by the centre are a unit of account that everyone recognises (1 token = 1 duty exemption).

when the tokens are passed through the population instead of being returned to the centre they create liquidity, they can be used in exchange for goods and effectively convey value between people (medium of exchange)

The key point here is that the centre issues tokens by spending and retires them by taxing, none else in the village can create the tokens (that would be counterfeit). At the same, everyone villagers accept the token as a means of payment because they know the centre will accept it back.

Money is created!

Key features of the two views

The table above summarises in 4 points the key features of the Modern Money view in comparison to the traditional view.

According to the traditional view (mainstream or orthodox view) money is a natural invention of the private society and arises to facilitate the exchanges of private actors. Since money is created from gold, it is essentially a commodity and successively, when the metal was replaced by bank notes, a convention.

The government plays a minor role in the money creation process, it is there only for technical support (coinage, lending of last resort).

According to the Modern Money view (heterodox), money is not something created by the private society seeking an efficient way for their exchange. Money is a constitutional project initiated by the government (the centre), it is a legal institution used to record debits and credits.

In this process the government has a primary role since it issues the money and creates a demand for it through taxation.

It is important to mention the fact that the Modern Money view is supported by historical and anthropological evidence while there is no evidence supporting the traditional barter and efficiency view.

For the past 4000 years, at least, we have had Modern Money.

(J. M. Keynes, “A Treatise on Money ”, 1930)

Why is money accepted?

The Modern Money approach to the historical evolution of money clearly identifies the government (the centre) as the main (and only) actor able to create money (by issuing tokens) and to enforce its acceptance (by requiring back the tokens in tax payments).

If we look at modern societies the process of money issue and acceptance is more or less the same, even if today money is almost entirely an entry on a data server rather than a token made of stone or wood (or gold).

We still need to give the answer to one simple yet fundamental question: What is money?

We will see the answer in a short while but first we need to take one step back. I could very well give you the answer now but that would inevitably create more questions. I believe we can easily ascertain what money really is by understanding why money is accepted.

Why does the private sector accept the currency issued by the government?

The government doesn’t threat to punish the population if they decide not to use the local currency. Someone can use a currency issued by another government to buy goods and services as long as the counterparty agrees on that, and it will be completely legal. So, if government money is universally accepted by the population living in that country it means that they know that money can be used in exchange for something else.

So, imagine you work in a book shop, a customer comes in, picks the last Lee Child’s Jack Reacher book from a shelf and approach the counter to pay. He gives you 9£, you give him a receipts and he leaves the shop.

You didn’t seem to have any issue accepting the 9£ in exchange for the book, which is not surprisingly since on the back of the book there was a price stamp that said “9£” and it was you that put the stamp on the book. So the customer simply gave you what you demanded for the books (“9£”).

Why did you price the book in British Pounds? You could have used Euro or Swedish Crown. Did the government explicitly force you to price your books in Pounds, certainly not. One possible answer is that you need Pounds because your favourite grocery store only accepts pounds, hence it is much easier for you to get the currency you will be needing for your spending. But then we could ask the grocery store owner the same thing and we will probably end up with a similar answer. The owner needs pounds because his wholesaler only accepts pounds. Then the wholesaler itself only accepts pounds and so does his supplier and so on.

It may sound reasonable to think that a currency is accepted because all the individuals included in a producer-consumer chain agreed to use it to settle their transactions.

Can we then affirm that a particular currency is accepted by the population because they know it can be used for commercial purpose (buy-sell gods and services)? In principle we could, but it’s a rather weak assumption and generates further questions. Which individual in the chain decides which currency is best to use? Is it the one buying from the grocery store or the store owner, or maybe is the wholesaler? What if there are several producer-consumer chains and for each of them the individuals therein choose a currency different from another chain? That would create a situation where several currencies coexist in the same country.

This accepted-because-is-accepted reasoning is clearly flawed and it won’t give us an answer of why a national currency is accepted by the population. There has to be “something” that only the sovereign currency can guarantee you.

Everyone can create money the problem is to get it accepted.

Hyman Minsky

What backs up modern money (sovereign money)?

- Reserves of metal: in a gold standard regime the money issued by governments is pegged to the value of gold reserves; money is accepted because it can be exchanged, at a fix rate, for gold. Historically, governments used to hold reserves of precious metals (namely silver or gold) against the national currency. In same cases the currency itself contained some of this precious metal, think about gold coins circulating during the Roman Empire for instance. It was thought that the population would have accepted the sovereign money since they knew they could always exchange it for gold or silver.

- Reserves of foreign currencies: similar to the gold standard regime, with the difference that the pegging is based on a foreign currency instead of a precious metal.

- Nothing (Fiat): the national currency is not backed by something, neither metal nor foreign currencies.

- Legal tender laws: money acceptance is imposed by law.

- Tax liabilities: money is accepted because it can be used in tax payments.

The history of the evolution of money according to the modern money view gives us the correct answer:

modern money is fiat, it is accepted because it can be used to clear tax liabilities.

What is money?

Government liability denominated in the national currency.

Taxes drive money!

A sovereign government doesn’t need reserves of gold, sovereign currencies or any legal tender laws in order to guarantee the acceptance of its currency. It is enough to impose a tax liability to be paid in the government’s own currency. The national currency issued by the government is the only thing accepted in tax payments hence the domestic non-government sector will need to obtain this currency to avoid penalties.

Let’s dissect the definition of money:

- Government: money is issued only by the central government. Other non-government actors, commercial banks above all, can also create mediums that are normally used for buying and selling stuff but they are “money things” (not money). Money things are all mediums that are commonly used as money but are not proper money, they lie one level below government money (we will delve into this later on).

- Liability: For the issuing government money is a liability, a debt to the non-government sector. This can be counter-intuitive to grasp at a first glance and it’s because of the special nature of the sovereign government: it issues a currency that can be used to make (tax) payment to itself.

But if money is a liability for the government and debit must be offset by credit, what is the offsetting asset in this case? It’s the tax credit against the non-government sector.

And on the non-government sector side? Money is the asset and the tax owed to the government is the liability.

- Denominated in the national currency: money is not the same as currency even though we often use the two terms as surrogate. Money is the record of the liability the government has to the private sector while currency is the unit of account (like a unit of measurement) which this liability is denominated in (namely British Pound, US Dollar, Japanese Yen and so on).

In the remaining of Part II and Part III we will explore in more details why money is a liability and how it is driven by taxation.

Money Theories and Regimes

Chartal Money

The modern definition of money that we will be using from now on is Chartal money, or Fiat.

Fiat currency: a currency issued by a central government, with no intrinsic value, un-pegged and non-convertible.

According to the Chartalist approach money has no intrinsic value (in contrast to Metalism), it is accepted because it can be used in tax payments.

Money is a creature of the State.

The Central Government has a central role in the creation of Chartal money:

- It chooses a Money of Account

- It imposes a tax liability (in the same account)

- It issues a currency that becomes the social unit of account

- The currency is the government’s liability (IOU)

- The government accepts the currency for tax payments

- Domestic stocks and flows are denominated in the national currency

Note!

It is irrelevant what the currency in question is made of, be it stone, paper, gold or a byte.

Chartalism and its influences

Georg Friedrich Knapp, in his book “The State Theory of Money” (1924), introduced the definition of Chartalism as opposition to Metalism and unveiled the mechanism for understanding modern money.

I included in the list below some of the fundamentals studies on money, a must-read for understanding the functioning of modern money:

- Alfred Mitchell-Innes: “Credit Theory of Money” (1914), integration State Theory of Money and Credit Theory of Money

- Johan M. Keynes: “A Treatise on Money” (1930), money and money-of-account

- Hyman Minsky: “Stabilizing an Unstable Economy” (1986), Endogeneity of money

- Abba Lerner: “Money as a Creature of the State” (1947), Functional Finance

- Geoffrey Ingham: “The Nature of Money” (2004), Credit Money and capitalism development

- Charles Goodhart: “Two concepts of money: implications for the analysis of optimal currency areas” (1998), One nation one currency.

Money and money things

People often make some confusion when considering money created from the central government and money created by private financial institutions (bank money) as the same thing.

Government money and bank money are not really alike, the former is money and the latter is money things.

Money → IOUs issued by the Central Government

Money Things → IOUs issued by the Non-Government sector

Nowadays we probably use money things much more often than money, almost all of our transactions are settled via credit/debit card or bank transfer, what we called bank money. It may sound strange but we are using money (the one issued by the government) less and less. We rarely have a direct monetary relation with the government, even when we pay taxes or receive some government benefit, and this is mainly due to the fact that private banks act as intermediaries between the private non-financial sector and the public sector.

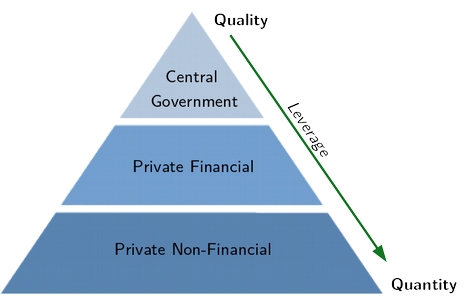

The figure below represents a 3-layers pyramid of liabilities. The acceptability of the liabilities issued by each level decreases as we move downward. IOUs issued by the private sector are less accepted than the ones issued by banks that are in turn less accepted than government IOUs.

Moreover, each level leverages the liabilities issued by the higher level that is why we have more private and bank liabilities in circulation than the government’s ones.

- Government IOUs are non convertible (fiat money).

- Private IOUs are convertible to government IOUs.

- Leveraging → small amount of government IOUs (Money) generates a wide range of Private IOUs (Money Things).

- Central Bank is the Lender of Last Resort.

Government IOUs are non convertible (fiat money).

Cash and reserves balance are the government IOUs, money, and in a fiat system, they are not convertible. If you hold a 100kr note you cannot go to the Swedish central bank and convert it to gold or to US dollars (at a fixed exchange rate), same for Dollar or Pound as well as any fiat currency. The only usage you can make out of your 100kr note is to to buy goods and services, pay taxes or make a deposit.

Mind that when I say convertible, I mean convertibility at fixed exchange rate, of course you can buy gold or dollar for the equivalent of 100kr depending on the market price

Private IOUs are convertible to government IOUs.

Bank money are private financial IOUs, money things, and contrary to government’s IOUs, they are convertible to money.

So, it is not correct to say that commercial banks create money, they create money things (bank money, one step below money).

If you have a deposit account at your bank with 1000£ on it, you hold 1000£ of money thing (your bank account is bank money); you don’t hold any cash you just have a positive number on your account. If you go to an ATM and withdraw 500£, you just converted 500 money things into money (in this case cash). The private bank liability is converted to government’s liability, and the money thing become money.

There is an important intermediate step that will be extensively covered in Part IV, when you take out cash from your account (or you make a bank transfer as we will see later), the bank must have enough reserves in order to convert the number 500 into real 500£.

Without those reserves you wouldn’t be able to receive your cash, and in an extreme case where your bank is not able to fund on the money market, the central bank needs step in as a lender of last resort and lend the needed reserves to your bank.

If we move to the bottom level of the pyramid, the private non-financial level, we can see an example of conversion from private non-financial IOUs to bank money.

You go to a car dealer to buy a car. You pay 10% of the price in cash and the remaining 90% is due in 60 days.

You just issued a private liability, or IOU. You got your car and paid 10% in cash and 90% in liability.

After 59 days you make a bank transfer from your checking account (a money thing) to the car seller’s account. What you did is a conversion, by converting your debt to the seller with a debt to the bank.

The private non-financial layer is now cleared, you have settled your debt using both money (the 10% cash) and money thing (the bank transfer, i.e. bank money).

Monetary regimes

Pegged exchange rate:

A country promises to redeem its currency for a commodity (usually gold) or another currency at a fixed exchange rate.

Managed exchange rate:

A country promises to redeem its currency at a floating exchange rate which is contained in a fixed exchange rate band.

Floating rate:

A country does not promise to redeem its currency at a fixed exchange rate.

Today most of the developed economies use fiat currencies, take for instance USA, Sweden, and United Kingdom, nonetheless there were and still are many situations where the nature of money had been altered. Before the end of the Bretton Woods system, developed economies were operating under a gold standard and today there are still governments that opted to peg their national currency to a foreign currency, or even more extreme to adopt a foreign currency as domestic social unit of account (Eurozone).

Monetary regimes and policy space

The adoption of a certain monetary regime has crucial effect on the domestic policy space of a country.

Floating rate:

- Most policy space

- No default risk on its own currency

- Unlimited spending possibility

- Inflation and depreciation arbitrary

Managed float:

- Less policy space

- Spending can affect exchange rate

Pegged exchange rate:

- Least policy space

- Spending constrained by exchange rate

- Default risk on domestic currency greater than 0.

Countries and monetary regimes

Down below I included a small list of countries grouped by their monetary regime, it is only an example but if you would like to see a full list of countries by exchange rate regime you can check this link.

* The Euro zone as a whole is a fiat currency system but each single Euro-country is subjected to a foreign currency regime, i.e. the most rigid form of pegging.

Countries adhering to the Euro zone gave up completely on their monetary sovereignty and became currency users instead of currency issuers.

Continue to Part III – Sovereign Government and Fiscal Policy:

After having defined what a (full) sovereign country is, we delve into the operations of spending, taxation and deficit in modern money environment.

References for Part II:

Desan, C., Making Money: Coin, Currency, and the Coming of Capitalism, Oxford University Press

Godley, W. and Lavoie, M. (2007) Monetary Economics: An Integrated Approach to Credit, Money, Income, Production and Wealth, New York: Palgrave Macmillan

Godley, W., 1996, Money, Finance and National Income Determination: An Integrated Approach. Levy Economics Institute, Working Paper 167, June, http://www.levy.org

Goodhart, C.A.E., 1989. Money, Information and Uncertainty Cambridge, MA: The MIT Press.

Knapp, Georg Friedrich. (1924) 1973. The State Theory Of Money. Clifon: Augustus M. Kelley.

Ingham, G., 2000. Babylonian Madness: On the Historical and Sociological Origins of Money. In John Smithin (ed.) What Is Money. London & New York: Routledge.

—, 2004a) “The Nature of Money,” Economic Sociology: European electronic newsletter, Vol 5 (2), January 2004, pp. 18-28.

—, 2004b. The Nature of Money, Cambridge: Polity Innes, A.M. (1913) What is Money? Banking Law Journal30(5): 377-408. Reprinted in

Wray, L. R. (ed.) Credit and State Theories of Money. Northampton: Edward Elgar. 2004.

Lerner A., 1947. Money as a Creature of the State, American Economic Review, 37(2), May, pp.312–17.

—.(1914) The Credit Theory of Money. Banking Law Journal31(2): 151–168. Reprinted in Wray, L. R. (ed.) Credit and State Theories of Money, 50-78. Northampton: Edward Elgar. 2004.

—, 1998. Understanding Modern Money: The Key to Full Employment and Price Stability. Northampton, MA, Edward Elgar.

—, 1990. Money and Credit in Capitalistic Economies: The Endogenous Money Approach. Aldershot, UK and Brookfield, VT, USA: Edward Elgar.

—. (2002) A Monetary Theory of Public Finance. International Journal of Political Economy 32 (3): 80-97.