Recap from part III – Sovereign Government and Fiscal Policy

In the previous part, Sovereign Government and Fiscal Policy, we have gone through the following topics:

- The sovereignty of a country and its monetary regime.

- Spending and taxation for sovereign countries

- Deficit spending policies

Highlight of part IV – Modern Monetary System:

This part is a bit more technical yet not difficult to understand. We go through the operations of money creation by both central banks and private banks.

We then look into the details on how the coordination between treasury and central bank works in practice.

Money creation and Reserves

Money and Interest rate

In the previous parts we have introduced and analysed the functioning of Modern Money or fiat currency. We have defined fiat currency as a floating currency (unpegged and non-convertible) with no intrinsic value.

We will now analyse in more details the functioning of a monetary system based on a floating exchange rate regime. The quantity of money and reserves, the interest rate and the role of the central bank is highly affected by the exchange rate regime.

The table above summarises the key differences in the quantity of money (M), the quantity of reserves (R) and Interest rate (I).

The orthodox school of macroeconomics is in favour of a fixed exchange regime where the quantity of money as well the reserves are fixed and determined by the central bank. The interest rate is then determined by the private actors competing for the fixed quantity of money.

This approach to monetary policy is usually referred as Exogenous money or Verticalism. Money is exogenous because the private sector has no control over the quantity which is instead fixed exogenously by the public sector (central bank or government).

We can notice one more time how the orthodox school applies to the real world and realises a certain approach to monetary policy:

Resources are scarce, money is a commodity hence it is scarce, only a fixed amount is available for the society.

The heterodox or Modern Money approach works the other way around, it is not the central bank that decides the quantity of money and reserves, the private financial sector does; the central bank can only set the interest rate target and accommodate the quantity of reserves in order to meet this target.

This approach is usually called Endogenous Money or Horizontalism since the private sector endogenously determines the quantity of money.

Money is not a commodity, it is nothing physical, it is a social unit of account hence virtually unlimited.

Endogenous Money and Interest Rate

The central bank independence is a myth…

- Endogenous money: money supply or bank reserves are determined by the system, the Central Bank accommodates the demand for reserves. The Central Bank does not control money supply, it can only control the price.

- Exogenous Interest Rate: the Central Bank sets the interest rate target and accommodates the demand for reserve accordingly.

- The Central Bank is not (and cannot be) independent: the central bank is a creature of the government and it is the bankers’ bank. The coordination between government and central bank is fundamental to guarantee the correct functioning of the payment system.

- Exchange rate as well as specific policies can affect the exogeneity of the target rate.

- Quantitative Easing*: the Central Bank buys securities and provides excess reserves to the banking system.

Treasury – Central Bank coordination

The Monetary Base

In the figure below we can see a, simplified, typical balance sheet of a central bank. We won’t go through each element in details but we will focus mainly on L1 and L2, since these are the elements composing the Monetary Base.

Particular focus will be put on the Reserves Balance (L2) since they are the key linkage between the central bank and the private banks, hence between the private and the public sector.

Reserves balance are, at all effect, a checking account of private banks at the central bank.

It is more or like the same relation between you and your bank, your checking account is an asset for you and a liability for your bank.

The Monetary Base is equal to the sum of L1 and L2:

L 1 + L 2 = A 1 + A 2 + A 3 + A 4 + A 5 − L 3 − L 4 − L 5

Let’s see two basic examples on how the monetary base can change, creation and destruction.

Creation of monetary base: an increase in the central bank assets.

In the example below we can see how the central bank balance sheet changes when it buys a bonds from a private bank, this is often the case of a quantitative easing.

The central bank buys bonds from a private bank, the bond is an assets and it increases the central bank existing assets (↑ A1).

The private bank receives reserves, from the central bank, in exchange of bonds. Reserve balances are an asset for the private bank and a liability for the central bank and they increase by an amount equal to bond purchase (↑ L2).

The bond purchase by the central bank increases the Reserve Balances (L2) and consequently the monetary base.

Destruction of monetary base: an increase in the central bank liabilities

A reduction of the monetary base occurs when either cash (L1) or reserves (L2) issued by the central bank decrease.

A typical operation that generate a reduction of central bank reserves is a tax settlement by the private sector.

The tax payment by a private actor generates an increase of the central debt to the treasury (↑ L3) offset by an equal reduction of reserves (↓ L2).

As we have seen in part III, taxes destroy private sector wealth by reducing the quantity of money in circulation.

The Balance Sheet of a Private Bank

In the previous chapter we have seen an example on how a typical balance sheet of a central bank is composed and how the monetary base is determined.

Before going through the balance of private banks it is important to understand that:

Reserve balance are a liability for the central bank and an asset for private banks.

Reserve balances are a sort of deposit account that private banks hold at the central bank. It is, conceptually, not very different from the deposit account you have at your bank, it is a credit (an asset) for you and a debit (a liability) for your bank.

Checking and Saving accounts are the money things or banks IOUs.

Reserve balances are deposit accounts at the Central Bank ( L2: Reserves balances ).

We will now explore the money creation process performed by private banks, having in mind that banks create money things and not proper money (see part II).

We need first to understand the Money Multiplier Theory, how it works in theory and in practice.

The Money Multiplier – In theory…

According to the Money Multiplier model, reserves balance finance banks balance sheet expansion by increasing the amount of excess reserves available to private banks.

The quantity of money created by banks (M) is equal to the monetary base (MB) times a factor m (the money multiplier)

M = m ∗ MB

The process that generates a credit expansion is the following:

↑ RB → ↑ ER → Loans & Deposits ↑ ⇒ Credit Expansion

The Central Bank increases the supply of reserves balance (↑ RB) which generates an increase in banks excess reserves (↑ ER); this allows banks to create more loans and deposits (Loans &Deposits ↑).

The Money Multiplier model gives an estimate of how much loans and deposits can increase due to an increase of RB and ER.

We can see how this approach is based on a fixed exchange rate environment where it is the central bank that exogenously increases the quantity of money in the private sector.

However, this is how it works in theory…

The Money Multiplier – In the real world…

In the real world the Money Multiplier (m) works the other way around.

The credit expansion by private banks comes first and only successively there is a demand of reserve balances:

⇒ Credit Expansion Loans → Deposits → ↑ RB MB = M/m

- Banks create loans which create deposits independent of reserves position

- Banks acquire reserves in the money market if:

- Banks have reserve requirements to meet

- Banks have to settle a payment (interbank settlement)

- Cash withdraw

- The Central Bank accommodates the demand of reserves whatever this is.

This approach reflects the Modern Money (heterodox) approach to money, the event that generated an increase in the quantity of money was endogenous to the private sector, the bank creating a loan. The central bank intervenes in a second stage.

Banks and Money Creation – The simplest case

Based on the definition of the real world money multiplier we will now look at a detailed, yet simple, example on how a private bank can create money things from nothing.

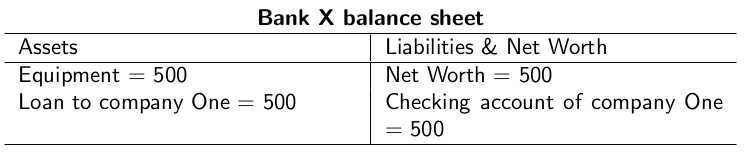

We start with a brand new bank, Bank X, that has just opened its business therefore no banking activities have been performed yet.

At the very beginning of its life the bank has only some equipment, we can assume it is an online-bank, and the relative net worth.

Good news for Bank X, the bank obtains its first customer, Company One, which would like to borrow 500 to finance a new machinery.

The bank run a risk assessment on the company and decide to grant it the loan of 500. The bank creates a new assets in its balance sheet, the loan to Company One, and at the same time the company obtains the required money via the checking account.

This operation generated one debit and one credit, the loan to the company is a credit for the bank while the checking account is a debit, the bank IOU.

The checking account is the money thing created by the bank.

How did Bank X generate the Money Things?

- The bank didn’t get the money from anywhere, the checking account to Company One was created from nothing.

- The bank didn’t need any existing deposit or cash.

- The bank is not lending anything it has.

- The money things created are the Bank IOUs.

The correct functioning of the banking operation has 2 requirements:

- Company One creditworthiness (ability to repay its loan).

- Bank X ability to acquire reserves in the eventuality of:

- Settlement of tax payments made by Company One.

- Interbank settlements (settle debit to other banks).

- Cash withdrawing by Company One

Banks and Money Creation – The role of reserves

Case 1: Interbank settlement

We start with the most common case that generates a demand of reserves by a financial institution, interbank settlement, and for doing this we continue with the simplest case introduced above.

Company One receives the invoice from the Supplier (of the machinery) and proceed with the payment by ordering Bank X to transfer 500 from his checking account to the supplier account.

If the supplier had a checking account in the same bank of Company One, Bank X, there would not be any need for reserve balances. Bank X would just mark up the supplier account and mark down Company One’s.

However, in this case the supplier has an account at another bank, Bank Y.

Bank X send the money thing to the supplier’s account at Bank Y, the checking account of Company One decreases (-500) and the checking account of the supplier increases (+500). Company One has done its job, the debt to the supplier is extinguished but the process is not completed.

Bank Y credit the supplier’s account but at the same time it is expected to receive the money from Bank X, it has a credit (a claim) to Bank X.

Bank X is short 500 of reserves to Bank Y and it needs to acquire these reserves in order to settle the interbank debt. The reserves are obtained from the central bank

Once Bank X obtains the needed reserves it can proceed with the interbank settlement and extinguish its debt to Bank Y.

At the end of the process we have the following positions:

- Bank X has a debit to the central bank due to the borrowed reserves and a credit to Company One for the loan.

- Bank Y credit the supplier’s account and receive the corresponding reserves

- The central bank has a claim on reserves to Bank X.

From this example we can see the fundamental role played by the central bank in a Modern Money (endogenous money) environment.

The central bank must accommodate for the demand of reserves, hence it doesn’t really have control over the quantity of money. Should the central bank not accommodate the required reserves the payment process would collapse.

What if the central bank sets a reserves requirement?

Such a measure requires private banks to hold a minimum amount of reserves at the the central bank for their lending activities. For example, if the reserves requirement is 1%, for every 100kr a bank lends it will need a positive reserves account at the central bank of 1kr.

The reserves needed to meet the requirement will be obtained in the money market at a rate that is usually higher than the one applied by the central bank.

Hence, the existence of reserves requirements, doesn’t affect the quantity of loans created by banks and the consequence demand of reserves. Banks create loans first and acquire the needed reserves afterwards, both for payment settlements and minimum reserves requirements.

This doesn’t mean that the reserves requirement has no effect on the lending activity; since the reserves are obtained in the interbank money market at a higher rate, the price of reserves is higher and, all else equal, the profitability of each loan decreases.

Reserves requirements don’t affect the demand of reserves but they do affect the price.

Banking and Reserves

The central bank has no control over the quantity of reserves, it controls only the price (at least in the short term).

- Banks use reserve balances to settle payments (consistently high % of GDP in modern economy)

- The central bank sets an interest rate target

- The central bank has to accommodate the demand for reserves in order to guarantee the correct functioning of the payment system (both infra-day and overnight)

- Reserve requirements do not affect supply/demand of reserve balances, only the price.

- Interbank lending does not change the total amount of reserves, it just changes the distribution of reserves

- Only the central bank can increase (or decrease) the amount of reserves at macro level. Interbank settlements operations do not affect the quantity of reserves available in the system.

Continue to Part V – Deficit Spending Arguments:

In this part we will address three arguments that commonly arise when dealing with deficit spending: Sustainability, Inflation and Exchange rate.

References for Part IV:

Fullwiler, S.T. (2006) Setting Interest Rates in the Modern Money Era, Journal of Post Keynesian Economics, 28 (3): 495–525.

—. (2009) The Social Fabric Matrix Approach to Central Bank Operations: An Application to the Federal Reserve and the Recent Financial Crisis. In Natarajan, Tara, Wolfram Elsner, and Scot Fullwiler, (eds.) Institutional Analysis and Praxis: The Social Fabric Matrix Approach,123-169. New York, NY: Springer.

—. (2011) Treasury Debt Operations: An Analysis Integrating Social Fabric Matrix

and Social Accounting Matrix Methodologies. Mimeograph.

—. (2013) “Modern Central Bank Operations: The General Principles.” In Basil Moore and Louis-Philippe Rochon (eds.), Post-Keynesian Monetary Theory and Policy: Horizontalism and Structuralism Revisited, Cheltenham: Edward Elgar.

Fullwiler, S.T, Kelton, S.A, and Wray, L.R., (2012) ‘Modern Money Theory: A Response to Critics, Political Economy Research Institute, Working Paper 279.

Marquis, M. (2002) Setting the Interest Rate, Federal Reserve Bank of San Francisco Economics Newsleter, No. 2002-30.